This printed article is located at https://qandm-dental.listedcompany.com/financials.html

Financials

Financials Archive![]() Note: Files are in Adobe (PDF) format.

Note: Files are in Adobe (PDF) format.

Please download the free Adobe Acrobat Reader to view these documents.

Condensed Financial Statement And Dividend Announcement For The Year Ended 31 December 2025

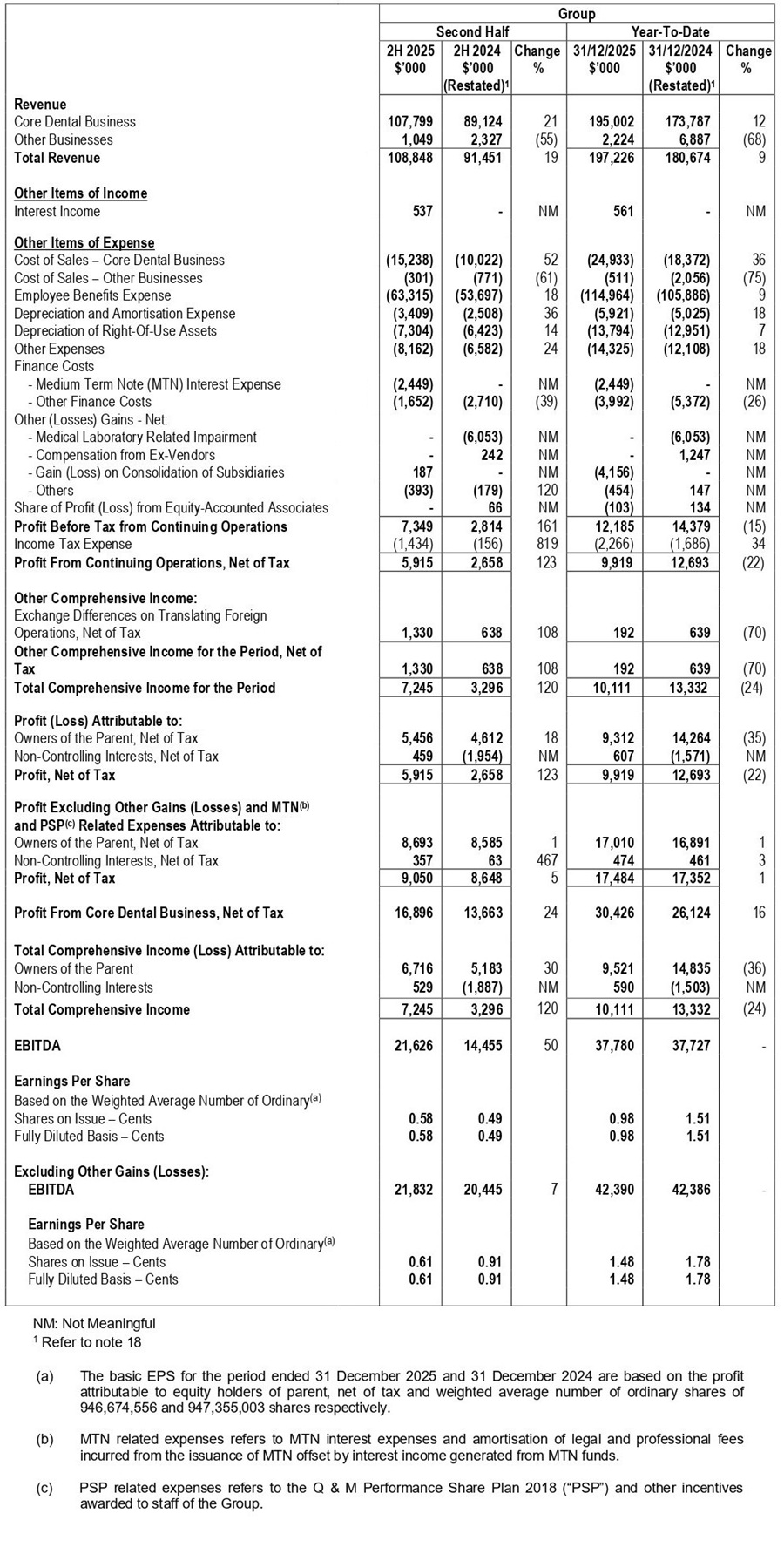

Condensed Interim Consolidated Statement of Profit or Loss and Other Comprehensive Income

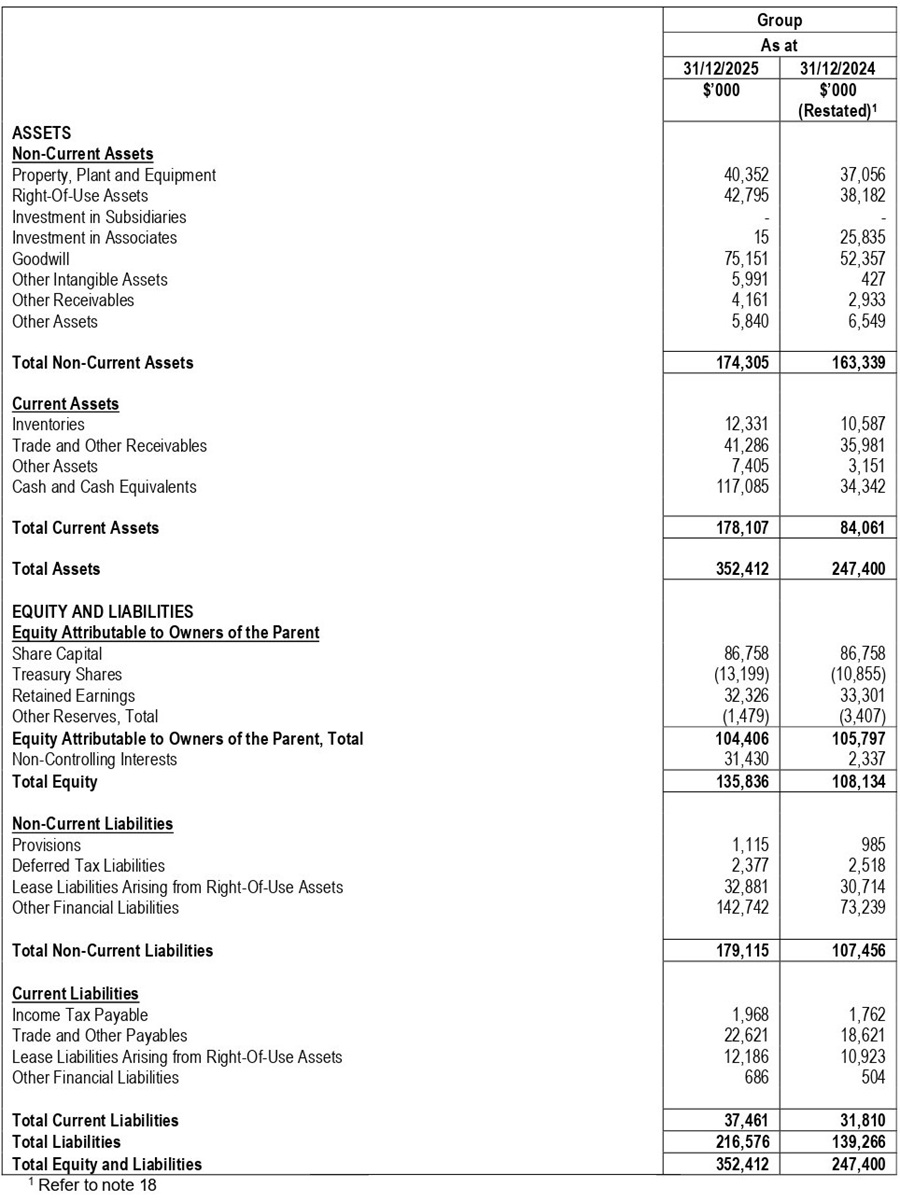

Condensed Interim Statements of Financial Position

Review of Performance

Statement of Comprehensive Income

Revenue

In Singapore, the Group has 110 dental outlets, 5 medical outlets, 1 dental college, 1 dental AI technology company and 1 dental equipment & supplies distribution company as at 31 December 2025 compared to 106 dental outlets, 5 medical outlets, 1 dental college, 1 dental AI technology company and 1 dental equipment & supplies distribution company as at 31 December 2024.

In Malaysia, the Group has 37 dental outlets and 1 dental equipment & supplies distribution company as at 31 December 2025 compared to 38 dental outlets and 1 dental equipment & supplies distribution company as at 31 December 2024.

In China, the Group has 7 dental polyclinics, 7 dental hospital, 5 dental training centres, 2 dental distribution & supplies companies and 3 dental laboratories as at 31 December 2025.

The revenue contribution from core dental business increased by 21% from $89.1 million for the six months ended 31 December 2024 (“2H24”) to $107.8 million for the six months ended 31 December 2025 (“2H25”). The increase of $18.7 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025 as well as increase in revenue contribution from Singapore dental clinics offset by reduction in profit guarantee income of $1.3 million.

The revenue contribution from other businesses decreased by 55% from $2.3 million in 2H24 to $1.0 million in 2H25. The decrease of $1.3 million was mainly due to the cessation of the Group’s medical laboratory in September 2024 due to the expiry of the clinical laboratory service licence.

The revenue contribution from core dental business increased by 12% from $173.8 million for the 12 months ended 31 December 2024 (“FY24”) to $195.0 million for the 12 months ended 31 December 2025 (“FY25”). The increase of $21.2 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025 as well as increase in revenue contribution from Singapore dental clinics offset by reduction in profit guarantee income of $1.4 million.

The revenue contribution from other businesses decreased by 68% from $6.9 million in FY2024 to $2.2 million in FY2025. The decrease of $4.7 million was mainly due to the cessation of the Group’s medical laboratory in September 2024 due to the expiry of the clinical laboratory service licence.

Other (Losses) Gains – Net

Net other losses amounting to $0.2 million in 2H25 was mainly due to plant and equipment written off due to the relocation of the Singapore head office in October 2025 offset by gain arising from the consolidation of EM2AI from equity-accounted associate to subsidiary of the Group.

Net other losses amounting to $6.0 million in 2H24 mainly due to impairment of goodwill, impairment on plant and equipment and impairment on inventories arising from the cessation of the Group’s medical laboratory in September 2024 due to the expiry of the clinical laboratory service licence.

Net other losses amounting to $4.6 million in FY25 was mainly due to the net loss arising from the deemed disposal of Aoxin Q & M and EM2AI when the Group gain control of these entities and reclassified them from equity-accounted associates to subsidiaries of the Group in 1H25 as well as plant and equipment written off due to the relocation of the Singapore head office in October 2025.

Net other losses amounting to $4.7 million in FY24 mainly due to impairment of goodwill, impairment on plant and equipment and impairment on inventories arising from the cessation of the Group’s medical laboratory in September 2024 due to the expiry of the clinical laboratory service licence offset by compensation from ex-vendors for the settlement and termination deed for Shanghai Chuangyi Investment & Management Co., Ltd. and ex-vendors from AR Dental Supplies Sdn. Bhd..

Other Items of Expense

Cost of Sales from Core Dental Business

Cost of sales from core dental business increased by 52% from $10.0 million in 2H24 to $15.2 million in 2H25. The increase of $5.2 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025.

As a percentage of revenue from the core dental business, cost of sales used in the core dental business in 2H25 was 14.1% compared to 11.2% in 2H24.

Comparing FY25 with FY24, cost of sales from core dental business increased 36% or $6.6 million mainly due to the same reason as given above.

As a percentage of revenue from the core dental business, cost of sales used in the core dental business in FY25 was 12.8% compared to 10.6% in FY24.

Cost of Sales from Other Businesses

The cost of sales from other businesses decreased by 61% from $0.8 million in 2H24 to $0.3 million in 2H25. The decrease of $0.5 million was mainly due to the cessation of the Group’s medical laboratory in September 2024.

As a percentage of revenue from other businesses, cost of sales used in other businesses in 2H25 was 28.7% compared to 33.1% in 2H24.

Comparing FY25 with FY24, cost of sales from other businesses decreased by 75% or $1.5 million mainly due to the same reason given above.

As a percentage of revenue from other businesses, cost of sales used in other businesses in FY25 was 23.0% compared to 29.9% in FY24.

Employee Benefits Expense

Employee benefits expense, which include professional fees paid to dentists, increased by 18% from $53.7 million in 2H24 to $63.3 million in 2H25. The increase of $9.6 million was mainly due to increase in revenue from the dental clinics in Singapore in 2H25, $0.7 million Q & M Performance Share Plan 2018 (“PSP”) and other incentives awarded to staff of the Group in 30 September 2025 for talent retention as well as the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025.

As a percentage of revenue, employee benefits expense in 2H25 was 58.2% compared to 58.7% in 2H24.

Comparing FY25 with FY24, employee benefits expense increased 9% or $9.1 million due to the same reasons given above.

As a percentage of revenue, employee benefits expense in FY25 was 58.3% compared to 58.6% in FY24.

Depreciation and Amortisation Expense

Depreciation and amortisation expense increased by 36% from $2.5 million in 2H24 to $3.4 million in 2H25. The increase of $0.9 million was mainly due to the consolidation of Aoxin Q & M and EM2AI from equity-accounted associates to subsidiaries of the Group in 1H25 offset by decrease in depreciation and amortisation as a result of the cessation of the Group’s medical laboratory in September 2024.

As a percentage of revenue, depreciation and amortisation expense in 2H25 was 3.1% compared to 2.7% in 2H24.

Comparing FY25 with FY24, depreciation and amortisation expense increased by 18% or $0.9 million due to the same reasons given above.

As a percentage of revenue, depreciation and amortisation expense in FY25 was 3.0% compared to 2.8 % in FY24.

Depreciation of Right-Of-Use (“ROU”) Assets

Depreciation of ROU assets increased by 14% from $6.4 million in 2H25 to $7.3 million in 2H25. The increase of $0.9 million was mainly due to the increase in dental clinics in Singapore and the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025 offset by the cessation of the Group’s medical laboratory in September 2024.

As a percentage of revenue, depreciation of ROU assets in 2H25 was 6.7% compared to 7.0% in 2H24.

Comparing FY25 with FY24, depreciation of ROU assets increased by 7% or $0.8 million due to the same reasons given above.

As a percentage of revenue, depreciation of ROU assets in FY25 was 7.0% compared to 7.2% in FY24.

Other Expenses

Other expenses increased by 24% from $6.6 million in 2H24 to $8.2 million in 2H25. The increase of $1.6 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in May 2025 and amortisation of legal and professional fees of $0.4 million incurred from the issuance of $130 million 3.95% notes on 10 July 2025 offset by the cessation of the Group’s medical laboratory in September 2024.

As a percentage of revenue, other expenses in 2H25 was 7.5% compared to 7.2% in 2H24.

Comparing FY25 with FY24, other expenses increased by 18% or $2.2 million due to the same reasons given above.

As a percentage of revenue, other expenses in FY25 was 7.3% compared to 6.7% in FY24.

Finance Costs

Finance costs increased by 51% from $2.7 million in 2H24 to $4.1 million in 2H25. The increase of $1.4 million was due to higher interest expense as a result of the issuance of $130 million 3.95% note on 10 July 2025.

As a percentage of revenue, finance costs in 2H25 was 3.8% compared to 3.0% in 2H24.

Comparing FY25 with FY24, finance costs increased by 20% or $1.1 million due to the same reason given above.

As a percentage of revenue, finance costs in FY25 was 3.3% compared to 3.0% in FY24.

Share of Profit from Equity-Accounted Associate

The Group recorded a share of profit from equity-accounted associates of $66k in 2H24 due to the share of profit from Aoxin Q & M offset by share of loss from EM2AI.

The Group recorded a share of loss from equity-accounted associates of $0.1 million in FY25 due a share of loss from EM2AI offset by a share of profit from Aoxin Q & M. EM2AI and Aoxin Q & M are now subsidiaries of the Group.

The Group recorded a share of profit from equity-accounted associates of $0.1 million in FY24 due to the share of profit from Aoxin Q & M offset by share of loss from EM2AI.

Profit Before Tax and Net Profit After Tax

The Group’s profit before tax increased from $2.8 million in 2H24 to $7.3 million in 2H25. The Group’s net after tax profit increased from $2.7 million in 2H24 to $5.9 million in 2H25.

Profit after tax attributable to owners of the parent increased from $4.6 million in 2H24 to $5.5 million in 2H25.

The Group’s net profit after tax decreased from $12.7 million in FY24 to $9.9 million in FY25.

Profit after tax attributable to owners of the parent decreased from $14.3 million in FY24 to $9.3 million in FY25.

Statement of Financial Position

As at 31 December 2025, the Group has cash and cash equivalents of $117.1 million while bank borrowings plus finance leases amounted to $143.4 million. As at 31 December 2024, the Group has cash and cash equivalents of $34.3 million while bank borrowings plus finance leases amounted to $73.7 million.

Current Assets

Inventory as at 31 December 2025 increased to $12.3 million from $10.6 million as at 31 December 2024. The increase of $1.7 million was due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in 2025.

Trade and other receivables as at 31 December 2025 increased to $41.3 million from $36.0 million as at 31 December 2024. The increase of $5.3 million was mainly attributable to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group and increase in trade receivables from Singapore dental clinics. This was partially offset by reclassification of the loan due from EM2AI, which is now recognised as a subsidiary receivable following the consolidation of EM2AI from an equity-accounted associate to a subsidiary in as well as decrease in profit guarantee receivable.

Other assets as at 31 December 2025 increased to $7.4 million from $3.2 million as at 31 December 2024. The increase of $4.2 million was mainly due capitalisation of legal and professional fees in connection with the drawdown of the Medium Term Note, increase in sign on bonus for dentists as well as ordinary shares awarded to employees in the Group in 2025 pursuant to the Q &M Performance Share plan 2018.

Non-Current Assets

The net book value of property, plant and equipment as at 31 December 2025 increased to $40.4 million from $37.1 million as at 31 December 2024. The increase of $3.3 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in 2025 offset by depreciation for plant and equipment.

The net book value of ROU assets as at 31 December 2025 increased to $42.8 million from $38.2 million as at 31 December 2024. The increase of $4.6 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group in 2025, opening of new clinics and renewal of ROU assets offset by depreciation of the ROU assets.

Investment in associates as at 31 December 2025 decreased to $15k from $25.8 million as at 31 December 2024. The decrease of $25.8 million due to the consolidation of Aoxin Q & M and EM2AI from equity-accounted associates to subsidiaries of the Group in 2025.

Goodwill as at 31 December 2025 increased to $75.2 million from $52.4 million as at 31 December 2024. The increase of $22.8 million was mainly due to the consolidation of Aoxin Q & M from equity-accounted associate to subsidiary of the Group in 2025.

Other intangible assets as at 31 December 2025 increased to $6.0 million from $$0.4 million as at 31 December 2024. The increase of $5.6 million was mainly due to the consolidation of Aoxin Q & M and EM2AI from equity-accounted associates to subsidiaries of the Group offset by amortisation of other intangible assets in 2025.

Other receivables as at 30 December 2025 increased to $4.2 million from $2.9 million in 31 December 2024. The increase of $1.3 million was due to loan to dentists offset by repayment of loan by the dentists of the Company.

Other assets as at 31 December 2025 decreased to $5.8 million from $6.5 million as at 31 December 2024. The decrease of $0.7 million was due to amortisation of sign on bonuses for dentists offset by increase in sign on bonuses for dentists.

Current Liabilities

Trade and other payables as at 31 December 2025 increased to $22.6 million from $18.6 million as at 31 December 2024. The increase of $4.0 million was mainly due to the consolidation of Aoxin Q & M and EM2AI from equity-accounted associates to subsidiaries of the Group in 2025 and accrual of MTN interest offset by payment of professional fees to dentists, doctors and staff bonuses which were accrued as at 31 December 2024.

Other financial liabilities as at 31 December 2025 increased to $0.7 million from $0.5 million as at 31 December 2024. The increase of $0.2 million was mainly due to bills payables from the dental equipment and supplies distribution company in Malaysia.

Lease liabilities from ROU assets as at 31 December 2025 increased to $12.2 million from $10.9 million as at 31 December 2024. The increase of $1.3 million was mainly due to the consolidation of Aoxin Q & M from an equity-accounted associate to a subsidiary of the Group, renewal of operating leases and opening of new clinics offset by repayment of operating lease.

Non-Current Liabilities

Other financial liabilities as at 31 December 2025 increased to $142.7 million from $73.2 million as at 31 December 2024. The increase of $69.5 million was mainly due to draw down of the Medium Term Note and bank loan offset by repayment of bank loan.

Statement of Cash Flows

The Group generated net cash flow from operating activities of $21.7 million in 2H25. This was mainly derived from operating cash flows before changes in working capital, increase of trade and other payables offset by increase in trade and other receivables and other nonfinancial assets in 2H25.

Net cash used in investing activities in 2H25 amounted to $6.4 million, mainly due to purchase of equipment for the existing and new dental clinics, acquisition of the remaining 51% of the entire issued and paid-up share capital of EM2AI and loan to dentists.

Net cash from financing activities in 2H25 was $54.8 million, mainly due to proceeds from Medium Term Note and proceeds from the right issue in Aoxin Q & M offset by repayment of bank loan and repayment of lease liabilities arising from right-of use assets.

Consequent to the above factors, the Group’s cash and cash equivalents was $117.1 million as at 31 December 2025.

Commentary

Industry Prospects

Barring any unforeseen circumstances, there are no known significant changes in the trends and competitive conditions of the industry in which the Group operates and no other major known factors or events that may adversely affect the Group in the next reporting period and the next 12 months.

Recent Developments and Future Plans

As part of its regional expansion strategy, the Group is actively pursuing strategic mergers and acquisitions across Singapore and the Asia Pacific region.

The Group intends to adopt a partnership-driven acquisition model, where consideration is structured as a combination of cash and equity. The equity component comprises shares in the Group, may be subject to moratorium provisions and multi-year service commitments to reinforce long-term stewardship and operational continuity. By participating in the broader value creation of the Group, including regional expansion initiatives and operational synergies, partners are incentivised to adopt a collective growth mindset and contribute to sustainable performance across all markets.

In respect of the People’s Republic of China (“PRC”), the Group intends to pursue expansion initiatives through its subsidiary, Aoxin Q & M, leveraging its established operating platform, local regulatory familiarity and network presence.

The Group notes the announced expansion plans of Aoxin Q & M to potentially deploy approximately RMB43.7 million (or S$8.0 million) towards acquisitions of established dental clinic chains outside North-Eastern China, as and when suitable targets are identified. These initiatives are aligned with the Group’s broader regional diversification strategy and disciplined capital allocation framework.

Notes

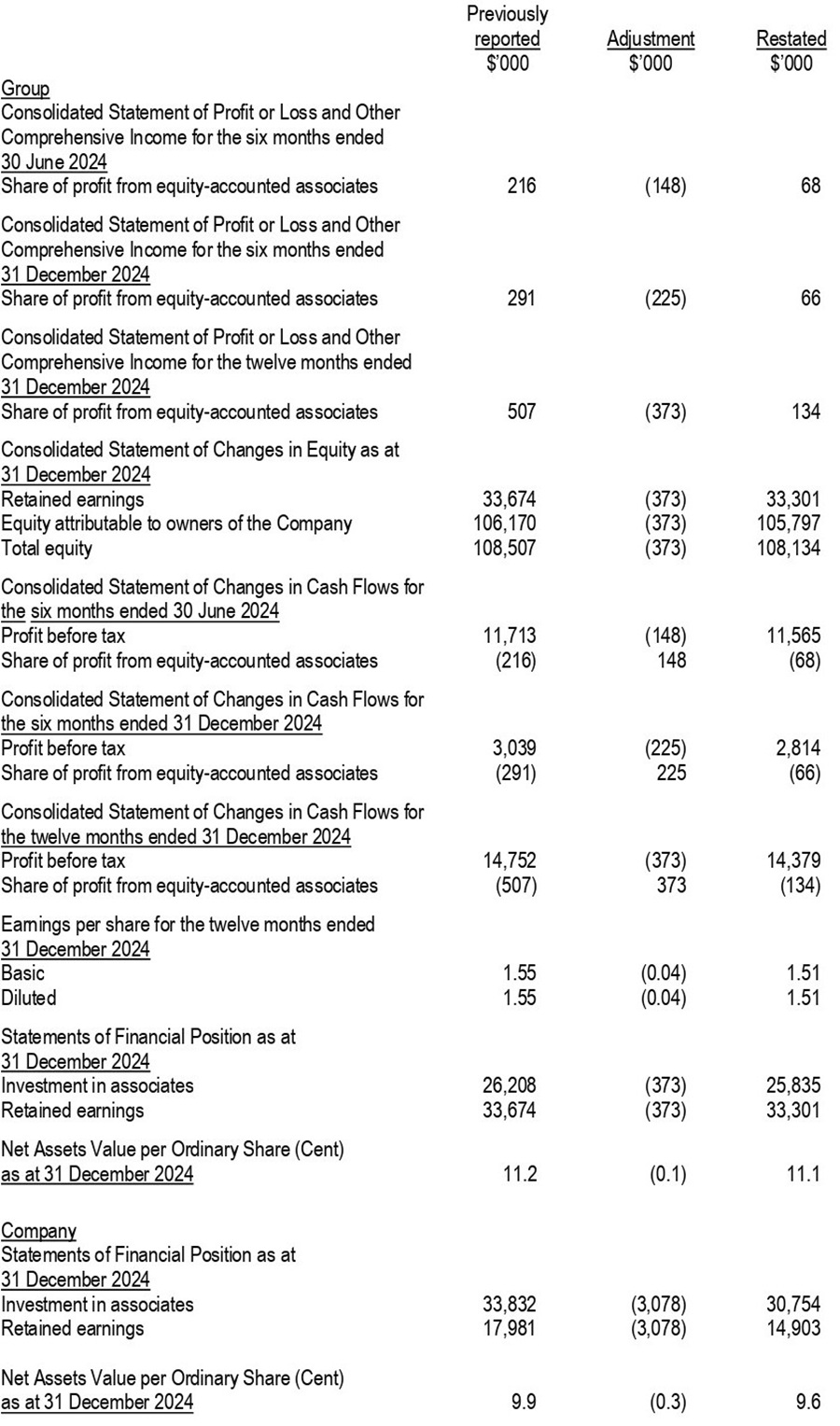

18. Restatement of prior financial statements

During the six months ended 30 June 2025, upon the request of the National Healthcare Security Administration 国家医疗保障局 (“NHSA”), a Chinese government agency that oversees, inter alia, the nation’s health insurance plan and centralized purchasing of drugs and medical supplies, Aoxin Q & M conducted a self-review exercise on two of the hospitals, namely Shenyang Aoxin Q & M Stomatology Hospital Co., Ltd. and Shenyang City Shenhe District No. 6 Hospital (Shenyang Aoxin Q & M Stomatology Hospital Co., Ltd. – Branch Hospital) (the “Hospitals”). Further to the self-review, NHSA and the Hospitals concluded that there was an excess claim of cost of material from NHSA amounting in aggregate to approximately RMB6.2 million for FY2024.

This overclaim resulted in an overstatement of revenue and understatement of liabilities in the twelve months period ended 31 December 2024 and an overstatement of the Company’s investment in associates. The overstatement of revenue and understatement of liabilities have been adjusted retrospectively by Aoxin Q & M. As a result, the Group’s consolidated statement of financial position, consolidated statement of profit or loss and other comprehensive income, consolidated statement of changes of equity, consolidated statement of cash flows and earning per share of the Group for 1H2024, 2H2024 and FY2024 and the Company’s statement of financial position and statement of changes in equity for FY2024 had since been restated.

The following table summarises the impact of the statement on the affected line items if 1H2024, 2H2024 and FY2024 financial statements: